Company type: auto-parts manufacturing with a heavy reliance on financing receivables

Length of fraud: from 2018 – 2025, declared bankruptcy in September 2025

Time to bankruptcy: 8 weeks from a failed $6.2 billion refinancing in August 2025 to bankruptcy

Total shortfall: $2.3 billion

Types of collateral: Invoice factoring, supply-chain financing

The collapse of First Brands Group represents one of the most significant alleged fraud events in private credit markets in recent years, with billions of dollars in exposure across banks, hedge funds, private credit funds, and supply chain finance providers.

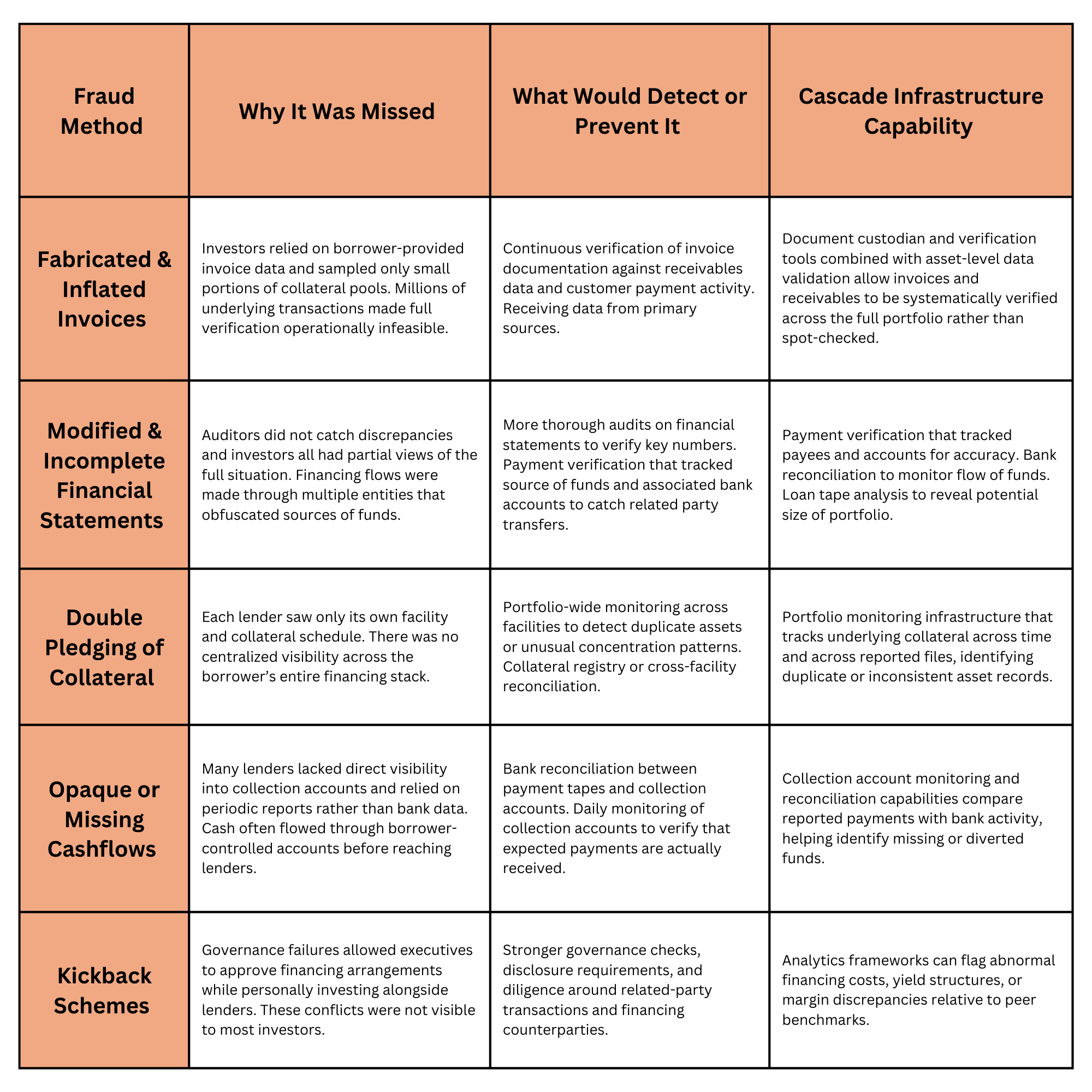

Fraud Mechanisms Identified

Investigations and court filings point to several mechanisms used to misrepresent collateral and extract financing.

Fabricated and Inflated Invoices

Prosecutors allege that First Brands fabricated invoices and inflated the value of legitimate invoices to obtain additional financing. In one documented example, a package of invoices worth $2.3 million was submitted with a value of $11.2 million, with some individual invoices inflated by 10x or more. Overall, roughly $2.7 billion in accounts receivable were fake or heavily manipulated at the time of bankruptcy.

How existing processes failed:

Supporting documentation was on a sample and aggregated: financing partners would ask for supporting documents on a sample of their loans but received aggregated invoices rather than the original individual invoices. These were fictitious because the individual invoices did not exist.

Audit discrepancies were ignored: During an audit in 2023, a financing partner requested documents for invoices they had purchased and received invoices that showed much lower amounts than First Brands had initially reported to them. The discrepancy was marked down as a mistake by a low-level employee.

Information came from only individuals involved in the scam: The one who had supplied documents in the case above was a lower-level employee, and afterwards the financing partner was directed to only request information from a circle of high-level employees that were in on the fraud.

How Cascade would have caught these issues:

Ongoing, complete loan verification: rather than the periodic spot checks performed by auditors or other service providers, Cascade checks every invoice or related document to an assigned receivable on an ongoing basis. There is no limit to the fields or number of documents that can be verified by Cascade, and they are done on the same day that loans are pledged to investors. This level of verification would have caught and flagged discrepancies much earlier in this case.

Data custodian tracking documents: Cascade can serve as a data custodian to store all related documents of pledged receivables. This would have caught any supporting documents that were missing but also avoided any reliance on aggregated invoices.

Checking meta-data on documents: Cascade can check meta-data related to the creation and modification timestamps of documents and PDFs. That would have flagged that many of the invoices provided here were created much after the original loans were supposed to be disbursed. This is also instrumental in catching fraudulent documents created by AI.

Transaction level payment reconciliation: Cascade can pull a full list of transactions from collection accounts and then reconcile them against payment tapes. Fraudulent invoices usually do not pay for long or have shortfalls, meaning Cascade could catch them if even a single payment is not matched.

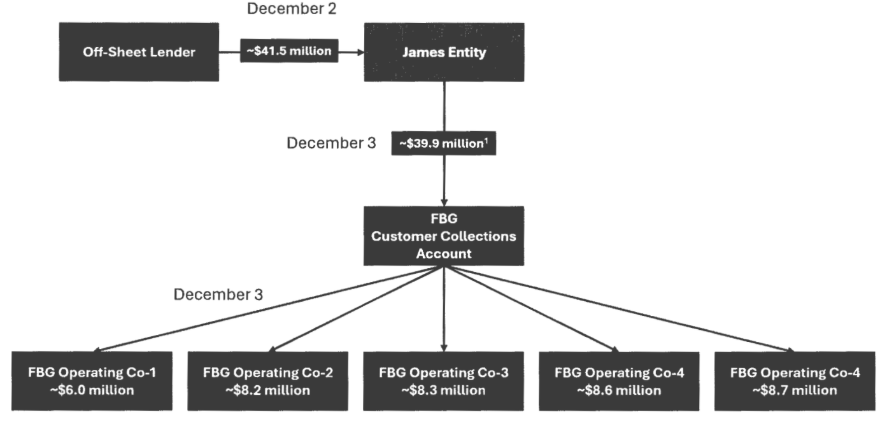

Modified and Incomplete Financial Statements

First Brands executives would modify consolidated financial statements to reflect a “fraction” of the real accounts payables and receivables financing they had received.

They also kept a lot of the financing completely off-balance sheet so that lenders would not know the scale of borrowing. This was accomplished with sale-leaseback arrangements using at least three connected entities. These entities would receive funds from the partner since they held the receivables but would funnel the cash and rights to the receivables back to First Brands. Amounts were sent to operating entities and made to look like they came from customers to avoid being seen as the related party transactions they were.

Below was an example of how funds flowed from a lender to the related entity to the master collections account and then to operating accounts:

How existing processes failed:

Not identifying source of payments: payments to collection accounts would consistently come from related entities rather than external customers. Despite the repeat payments from these entities, lenders did not suspect that the payments were from related parties. In fact, most lenders did not even know that these related entities existed.

Financial audits not catching manual adjustments: financials were falsified by teams at First Brands who maintained “bridge” files that would help maintain the real set of books with the fake books being reported to investors. Some adjustments were set numbers every time, which over multiple statements could have been seen as an odd pattern.

How Cascade would have caught these issues:

Payment verification on additional fields: Cascade’s payment verification is comprehensive and can capture fields beyond typical payment verifiers. One of the fields monitored would have been payee names and bank accounts, which would have flagged that these related entities were the ones paying instead of a wider variety of customer accounts.

Bank account verification and reconciliation: Cascade can also tie designated bank account numbers to specific borrowers, flagging if payments are coming from accounts that do not match during the payment reconciliation process.

Reconciling multiple sources of data: while Cascade does not fully rebuild financials from ledgers (yet), it can reconcile against major items on the balance sheet including the size of facilities. This is done by requesting a master tape of receivables to measure the full size of the portfolio versus what is reported on the financial statements. Even if this is only received during the diligence process, it should give clues to the true size of the loan portfolio and raise flags if that amount does not match against known funding facilities.

Forensic accounting fraud techniques: Cascade can apply techniques used in forensic accounting, such as checks based on Benford’s Law, to raise flags on whether data tapes or financials are unusual.

Double Pledging of Collateral

Executives are accused of pledging the same receivables and loan collateral multiple times across different financing facilities. This practice allowed the company to raise funding from multiple lenders using the same underlying assets. Such schemes are difficult to detect when lenders have visibility only into their own facility and there is no centralized monitoring of the full collateral pool.

How existing processes failed:

Lenders not aware of each other: diligence processes did not reveal that there were many off-balance sheet lenders financing First Brands. Instead, most lenders had no idea the extent of financing.

Lenders had limited views of the portfolio: lender reporting requirements did not involve seeing the full loan portfolio, only the portfolio that they were funding. This made it difficult to see if receivables were pledged to multiple parties.

How Cascade would have caught these issues:

Track collection account leakage: collateral that is pledged to multiple parties will usually not be able to be paid for long. Cascade can plug directly into bank collection accounts to reconcile them against reported inflows in data tapes. Even if receivables have been pledged to multiple parties, ensure that your collection account is the one receiving funds from them. Eg. If $1m in payments should have been made according to loan tapes, Cascade can check if $1m in payments were received in collection accounts.

Payment reconciliation: related to tracking leakage is to track every underlying payment into the collection account since double pledged collateral often does not pay for long. The moment payments are missed the investor can be alerted.

Historical borrowing base pledge checks: Cascade can rebuild all borrowing base and collateral reports over history using data tapes. This allows it to flag if loans are repeatedly pledged, or do not match the usual cadence between disbursement and assignment to SPVs.

Have visibility on the full portfolio or multiple deals: Cascade’s systems will automatically flag if a loan is either not unique or being assigned to multiple investors. Even if Cascade is not serving on multiple debt facilities, some investors have requested full loan tapes as a reporting requirement, allowing Cascade to do the same checks.

Opaque or Missing Cashflows

One of the most troubling aspects of the case involves missing or unaccounted-for cash flows. Court filings suggest that approximately $2.3 billion in receivable payments cannot be fully traced.

Even at the height of the bankruptcy, when lenders asked whether funds had been transferred to segregated collection accounts, First Brands’ counsel reportedly responded:

“We don’t know.” “US$0.”

First Brands also used “round-tripping”, where they would pay off delinquent invoices using funds from elsewhere to make it appear that customers were paying.

How existing processes failed:

Lack of control of collection accounts: First Brands was able to direct funds in and out of accounts it controlled with little oversight by lenders. It seems that there were few checks before wires were authorized.

Lenders did not track usage of funds: executives at First Brands would routinely funnel funds to themselves. While most of these were done through third party payment processing companies, there seemed to be few checks on source or destination of funds from there.

How Cascade would have caught these issues:

External cash management: collection accounts could have been controlled by third-party cash agents to prevent unauthorized cash outflows. Cascade often works with trustees, cash agents, and other service providers to give them the context they need to process requests swiftly. This includes checking for borrowing base deficiencies, covenant breaches, and verifying collateral pledges so that funds are not released if they should not be.

Daily visibility on deal status: a major reason investors allow for funds to be released, including from pre-funding deals or doing cash sweeps, is to not cripple the day-to-day operations of the borrower. Traditionally checks and reporting incurred delays that could stretch to a week, which puts pressure on investors to allow for some wires to be sent out more quickly. Cascade’s platform updates borrowing bases, covenants, and other key calculations on a daily basis, allowing for no delays and more oversight on funds being released.

Verification and reconciliation: the loan verification and payment reconciliation processes previously described would have caught this earlier as well.

Kickback Schemes

One of the main financiers to First Brands, Onset Financial, is alleged to have had a kickback scheme arranged with a First Brands VP (who was also brother to the CEO). Onset would provide short-tern loans with upfront payments that had up to 300% IRRs, then divert some of those profits to the brother. Onset was reported to have lent out $2.5 billion and received $2.9 billion from these deals. According to a January 9 lawsuit, he expected to earn approximately $130 million in profit from these investments.

Some employees were aware that something was off. In a September 2022 message sent days after Edward James agreed to an inventory loan with an alleged 179% internal rate of return, a First Brands employee wrote “‘dude .. whoever sold that onset deal to us is [Onset] employee of the century,’”

How existing processes failed:

Lack of governance: no employees should be able to invest in outside deals related to the company, but there were no checks and balances here. There also seemed to be no whistleblowing to alert outsiders about this deal.

Lack of diligence on other lenders: given the size of the financing from Onset, diligence should have revealed this business arrangement. A relatively unknown, mid-sized equipment leasing and finance firm in Utah doing $2.5 billion in deals would have seemed off.

How Cascade would have caught these issues:

Data Validation: Cascade can stratify loans by product type, issuer, or other metrics and would have caught how different and off market these loans were. However, it is unlikely that these loans would have been disclosed to any investors so this is an issue that can largely be caught through more thorough diligence.

Checklist of Red Flags

In hindsight, several indicators suggested areas of potential suspicion:

Structural Complexity Did Not Match Operations: payments went through a convoluted flow of funds involving multiple entities. This is more common in deals with multiple debt facilities but most lenders allegedly did not know of the existence of other facilities. The existence of those operational flows should have tipped off there was more than met the eye.

Margin Expansion Diverging From Industry Norms: First Brands reported margins significantly higher than industry peers.

Extreme Reliance on Factoring: Approximately 70% of revenues were derived from factoring payments, creating a heavy dependence on receivables financing despite First Brands not being a financing company first

Deals Too Good To Be True: Some financing arrangements carried interest rates exceeding 30%, an unusually high cost for a supposedly investment-grade receivables structure.

Documentation Resistance: Multiple lenders reported difficulty obtaining satisfactory answers to documentation requests, including receiving aggregated reports.

Poor Governance: communication channels were exclusively through top management involved in fraud, and lenders were kept in the dark on many issues on the deal

Cascade Principles of Fraud Mitigation

Fraud in ABL transactions can usually be found in three main areas:

False data: misrepresented data or payment tapes, false bank transactions, etc.

False documents: generated or modified documents tied to receivables, payments, etc.

False claims:overstating / understating performance, creating entities to cover their tracks, etc.

To mitigate fraud, Cascade is guided by three main principles:

Systematic vs Spot checks: Cascade systematically verifies or reconciles every receivable and transaction rather than performing spot checks like most traditional providers.

First Principles Approach: Cascade takes raw data straight from the source where possible, then recalculates or extracts key values rather than taking any submissions at face value.

Multiple Layers of Protection: No process is foolproof, but by combining multiple methods of mitigating fraud, Cascade can achieve an outcome that is greater than the sum of its parts. Cascade’s product offering can also be used selectively to fill in only where there are gaps in existing processes.

Cascade’s Deal Infrastructure suite was created specifically to mitigate fraud on deals and includes:

Data Custodian

Loan Verification

Payment Reconciliation

Collateral Verification

Collateral Registration

Cash Monitoring & Sweeping

Back-up Servicing

For more information, check out the one-pager at the link here.

Company type: auto-parts manufacturing with a heavy reliance on financing receivables

Length of fraud: from 2018 – 2025, declared bankruptcy in September 2025

Time to bankruptcy: 8 weeks from a failed $6.2 billion refinancing in August 2025 to bankruptcy

Total shortfall: $2.3 billion

Types of collateral: Invoice factoring, supply-chain financing

The collapse of First Brands Group represents one of the most significant alleged fraud events in private credit markets in recent years, with billions of dollars in exposure across banks, hedge funds, private credit funds, and supply chain finance providers.

Fraud Mechanisms Identified

Investigations and court filings point to several mechanisms used to misrepresent collateral and extract financing.

Fabricated and Inflated Invoices

Prosecutors allege that First Brands fabricated invoices and inflated the value of legitimate invoices to obtain additional financing. In one documented example, a package of invoices worth $2.3 million was submitted with a value of $11.2 million, with some individual invoices inflated by 10x or more. Overall, roughly $2.7 billion in accounts receivable were fake or heavily manipulated at the time of bankruptcy.

How existing processes failed:

Supporting documentation was on a sample and aggregated: financing partners would ask for supporting documents on a sample of their loans but received aggregated invoices rather than the original individual invoices. These were fictitious because the individual invoices did not exist.

Audit discrepancies were ignored: During an audit in 2023, a financing partner requested documents for invoices they had purchased and received invoices that showed much lower amounts than First Brands had initially reported to them. The discrepancy was marked down as a mistake by a low-level employee.

Information came from only individuals involved in the scam: The one who had supplied documents in the case above was a lower-level employee, and afterwards the financing partner was directed to only request information from a circle of high-level employees that were in on the fraud.

How Cascade would have caught these issues:

Ongoing, complete loan verification: rather than the periodic spot checks performed by auditors or other service providers, Cascade checks every invoice or related document to an assigned receivable on an ongoing basis. There is no limit to the fields or number of documents that can be verified by Cascade, and they are done on the same day that loans are pledged to investors. This level of verification would have caught and flagged discrepancies much earlier in this case.

Data custodian tracking documents: Cascade can serve as a data custodian to store all related documents of pledged receivables. This would have caught any supporting documents that were missing but also avoided any reliance on aggregated invoices.

Checking meta-data on documents: Cascade can check meta-data related to the creation and modification timestamps of documents and PDFs. That would have flagged that many of the invoices provided here were created much after the original loans were supposed to be disbursed. This is also instrumental in catching fraudulent documents created by AI.

Transaction level payment reconciliation: Cascade can pull a full list of transactions from collection accounts and then reconcile them against payment tapes. Fraudulent invoices usually do not pay for long or have shortfalls, meaning Cascade could catch them if even a single payment is not matched.

Modified and Incomplete Financial Statements

First Brands executives would modify consolidated financial statements to reflect a “fraction” of the real accounts payables and receivables financing they had received.

They also kept a lot of the financing completely off-balance sheet so that lenders would not know the scale of borrowing. This was accomplished with sale-leaseback arrangements using at least three connected entities. These entities would receive funds from the partner since they held the receivables but would funnel the cash and rights to the receivables back to First Brands. Amounts were sent to operating entities and made to look like they came from customers to avoid being seen as the related party transactions they were.

Below was an example of how funds flowed from a lender to the related entity to the master collections account and then to operating accounts:

How existing processes failed:

Not identifying source of payments: payments to collection accounts would consistently come from related entities rather than external customers. Despite the repeat payments from these entities, lenders did not suspect that the payments were from related parties. In fact, most lenders did not even know that these related entities existed.

Financial audits not catching manual adjustments: financials were falsified by teams at First Brands who maintained “bridge” files that would help maintain the real set of books with the fake books being reported to investors. Some adjustments were set numbers every time, which over multiple statements could have been seen as an odd pattern.

How Cascade would have caught these issues:

Payment verification on additional fields: Cascade’s payment verification is comprehensive and can capture fields beyond typical payment verifiers. One of the fields monitored would have been payee names and bank accounts, which would have flagged that these related entities were the ones paying instead of a wider variety of customer accounts.

Bank account verification and reconciliation: Cascade can also tie designated bank account numbers to specific borrowers, flagging if payments are coming from accounts that do not match during the payment reconciliation process.

Reconciling multiple sources of data: while Cascade does not fully rebuild financials from ledgers (yet), it can reconcile against major items on the balance sheet including the size of facilities. This is done by requesting a master tape of receivables to measure the full size of the portfolio versus what is reported on the financial statements. Even if this is only received during the diligence process, it should give clues to the true size of the loan portfolio and raise flags if that amount does not match against known funding facilities.

Forensic accounting fraud techniques: Cascade can apply techniques used in forensic accounting, such as checks based on Benford’s Law, to raise flags on whether data tapes or financials are unusual.

Double Pledging of Collateral

Executives are accused of pledging the same receivables and loan collateral multiple times across different financing facilities. This practice allowed the company to raise funding from multiple lenders using the same underlying assets. Such schemes are difficult to detect when lenders have visibility only into their own facility and there is no centralized monitoring of the full collateral pool.

How existing processes failed:

Lenders not aware of each other: diligence processes did not reveal that there were many off-balance sheet lenders financing First Brands. Instead, most lenders had no idea the extent of financing.

Lenders had limited views of the portfolio: lender reporting requirements did not involve seeing the full loan portfolio, only the portfolio that they were funding. This made it difficult to see if receivables were pledged to multiple parties.

How Cascade would have caught these issues:

Track collection account leakage: collateral that is pledged to multiple parties will usually not be able to be paid for long. Cascade can plug directly into bank collection accounts to reconcile them against reported inflows in data tapes. Even if receivables have been pledged to multiple parties, ensure that your collection account is the one receiving funds from them. Eg. If $1m in payments should have been made according to loan tapes, Cascade can check if $1m in payments were received in collection accounts.

Payment reconciliation: related to tracking leakage is to track every underlying payment into the collection account since double pledged collateral often does not pay for long. The moment payments are missed the investor can be alerted.

Historical borrowing base pledge checks: Cascade can rebuild all borrowing base and collateral reports over history using data tapes. This allows it to flag if loans are repeatedly pledged, or do not match the usual cadence between disbursement and assignment to SPVs.

Have visibility on the full portfolio or multiple deals: Cascade’s systems will automatically flag if a loan is either not unique or being assigned to multiple investors. Even if Cascade is not serving on multiple debt facilities, some investors have requested full loan tapes as a reporting requirement, allowing Cascade to do the same checks.

Opaque or Missing Cashflows

One of the most troubling aspects of the case involves missing or unaccounted-for cash flows. Court filings suggest that approximately $2.3 billion in receivable payments cannot be fully traced.

Even at the height of the bankruptcy, when lenders asked whether funds had been transferred to segregated collection accounts, First Brands’ counsel reportedly responded:

“We don’t know.” “US$0.”

First Brands also used “round-tripping”, where they would pay off delinquent invoices using funds from elsewhere to make it appear that customers were paying.

How existing processes failed:

Lack of control of collection accounts: First Brands was able to direct funds in and out of accounts it controlled with little oversight by lenders. It seems that there were few checks before wires were authorized.

Lenders did not track usage of funds: executives at First Brands would routinely funnel funds to themselves. While most of these were done through third party payment processing companies, there seemed to be few checks on source or destination of funds from there.

How Cascade would have caught these issues:

External cash management: collection accounts could have been controlled by third-party cash agents to prevent unauthorized cash outflows. Cascade often works with trustees, cash agents, and other service providers to give them the context they need to process requests swiftly. This includes checking for borrowing base deficiencies, covenant breaches, and verifying collateral pledges so that funds are not released if they should not be.

Daily visibility on deal status: a major reason investors allow for funds to be released, including from pre-funding deals or doing cash sweeps, is to not cripple the day-to-day operations of the borrower. Traditionally checks and reporting incurred delays that could stretch to a week, which puts pressure on investors to allow for some wires to be sent out more quickly. Cascade’s platform updates borrowing bases, covenants, and other key calculations on a daily basis, allowing for no delays and more oversight on funds being released.

Verification and reconciliation: the loan verification and payment reconciliation processes previously described would have caught this earlier as well.

Kickback Schemes

One of the main financiers to First Brands, Onset Financial, is alleged to have had a kickback scheme arranged with a First Brands VP (who was also brother to the CEO). Onset would provide short-tern loans with upfront payments that had up to 300% IRRs, then divert some of those profits to the brother. Onset was reported to have lent out $2.5 billion and received $2.9 billion from these deals. According to a January 9 lawsuit, he expected to earn approximately $130 million in profit from these investments.

Some employees were aware that something was off. In a September 2022 message sent days after Edward James agreed to an inventory loan with an alleged 179% internal rate of return, a First Brands employee wrote “‘dude .. whoever sold that onset deal to us is [Onset] employee of the century,’”

How existing processes failed:

Lack of governance: no employees should be able to invest in outside deals related to the company, but there were no checks and balances here. There also seemed to be no whistleblowing to alert outsiders about this deal.

Lack of diligence on other lenders: given the size of the financing from Onset, diligence should have revealed this business arrangement. A relatively unknown, mid-sized equipment leasing and finance firm in Utah doing $2.5 billion in deals would have seemed off.

How Cascade would have caught these issues:

Data Validation: Cascade can stratify loans by product type, issuer, or other metrics and would have caught how different and off market these loans were. However, it is unlikely that these loans would have been disclosed to any investors so this is an issue that can largely be caught through more thorough diligence.

Checklist of Red Flags

In hindsight, several indicators suggested areas of potential suspicion:

Structural Complexity Did Not Match Operations: payments went through a convoluted flow of funds involving multiple entities. This is more common in deals with multiple debt facilities but most lenders allegedly did not know of the existence of other facilities. The existence of those operational flows should have tipped off there was more than met the eye.

Margin Expansion Diverging From Industry Norms: First Brands reported margins significantly higher than industry peers.

Extreme Reliance on Factoring: Approximately 70% of revenues were derived from factoring payments, creating a heavy dependence on receivables financing despite First Brands not being a financing company first

Deals Too Good To Be True: Some financing arrangements carried interest rates exceeding 30%, an unusually high cost for a supposedly investment-grade receivables structure.

Documentation Resistance: Multiple lenders reported difficulty obtaining satisfactory answers to documentation requests, including receiving aggregated reports.

Poor Governance: communication channels were exclusively through top management involved in fraud, and lenders were kept in the dark on many issues on the deal

Cascade Principles of Fraud Mitigation

Fraud in ABL transactions can usually be found in three main areas:

False data: misrepresented data or payment tapes, false bank transactions, etc.

False documents: generated or modified documents tied to receivables, payments, etc.

False claims:overstating / understating performance, creating entities to cover their tracks, etc.

To mitigate fraud, Cascade is guided by three main principles:

Systematic vs Spot checks: Cascade systematically verifies or reconciles every receivable and transaction rather than performing spot checks like most traditional providers.

First Principles Approach: Cascade takes raw data straight from the source where possible, then recalculates or extracts key values rather than taking any submissions at face value.

Multiple Layers of Protection: No process is foolproof, but by combining multiple methods of mitigating fraud, Cascade can achieve an outcome that is greater than the sum of its parts. Cascade’s product offering can also be used selectively to fill in only where there are gaps in existing processes.

Cascade’s Deal Infrastructure suite was created specifically to mitigate fraud on deals and includes:

Data Custodian

Loan Verification

Payment Reconciliation

Collateral Verification

Collateral Registration

Cash Monitoring & Sweeping

Back-up Servicing

For more information, check out the one-pager at the link here.

%20(5%20x%202%20in).png)